Financial Markets&Institutions - Chapter 2: Bond Markets Özeti :

PAYLAŞ:Chapter 2: Bond Markets

Characteristics and Types of Bonds

Bond is a long-term financial instrument issued by companies or governments, which provides interest and principal payments to the holders on specific dates. It is issued to satisfy long term financing needs, and is suitable for companies especially which do not want to lose management of the company by issuing stocks.

There are two main participants of the bond markets. The first group is the borrowers. Borrowers are the bond issuers such as governments, municipalities, financial and real sector companies. The second group is the bond investors or holders. They are the institutions or individuals who want to evaluate their savings in the bond markets. By purchasing bonds, they lend their savings to the borrowers in need of funds.

Although bond is a type of debt financing, differently from the bank loans, it is traded in secondary markets. The most traded type of bonds is the bond that makes regular interest payments and principal payment on the maturity date, which is called conventional bond. Bonds are redeemed on a specified date. However, based on their type, they can also be redeemed on a specified date when a predetermined event occurs or at some time in between two dates. If it is a callable bond, then it will be redeemed when the company calls the bonds.

There are some elements that determine the characteristics of the bonds. These are:

Par value,

- Form of the bond (Bearer or registered)

- Payment method (Coupon or discount)

- Coupon payment frequency (annually, semiannually, quarterly or monthly)

- Maturity,

- Call feature if it is callable,

- Sinking fund if it is a sinking fund bond,

- Creditworthiness of the issuer

Principal or Par Value: The principal, which is also referred to as par value, redemption value or maturity value, is the amount that the issuer agrees to repay on the maturity date.

Coupon Payments: Most of the bonds make regular payments to the holders, which is called coupon or interest payment. The amount of the payments is initially specified as an annual Bond is a fixed-income security and a type of debt instrument. 32 Bond Markets percentage of the principal (fixed-rate bonds) or as a floating rate, which depends on an external measure such as LIBOR (London Interbank Offered Rate), inflation, currency and gold.

Maturity: Bonds are issued with a maturity date. Maturity or term of a bond is the number of years that the issuer meets the obligations of the bond, and refers to a specified date on which par value (principal) of the bond must be repaid to the holder. As the maturity of a bond increases, the price volatility of the bond will increase due to the changes in market yields.

Bonds are classified in several ways. The type of a bond that will be issued is determined depending on the needs of issuer and demand of the investors, and each type is suitable for different types of investors based on its features. Some issuers want to reduce the borrowing costs and issue bonds with collateral. Some issuers do not want to provide collateral, so they issue debentures and accept to pay a higher interest rate.

Some types of bonds are:

Bearer and Registered Bonds: Bonds are divided into two categories in terms of ownership: bearer bonds and registered bonds. Bearer bond is a bond type that the owner is the person who holds it. They have coupons that are presented to a bank for payment. The issuer of the bearer bonds does not know the holder of the bond and who receives the cash flows of the bond. As opposed to bearer bonds, the issuer of the registered bonds knows the names of the holders and payments are made directly to the holders.

Straight Coupon Bonds: The most common type of bonds traded in the markets is straight coupon bonds, which provide the holder to receive periodic interest payments and principal on a specified date. The interest payments of these bonds are generally made annually or semiannually, and neither the issuer nor the investor have the right of demanding early repayment.

Zero-Coupon (Discounted) Bonds: Holders of zero-coupon bonds do not receive coupon payments. They buy the bond at a discounted price, and they receive the par value at the maturity. The difference between the discounted price and the par value becomes the interest payment of the bondholders. The reason why companies issue zero coupon bonds is that they do not have to make payment until the maturity date, and the reason investors prefer this type of bond is that there is no risk of reinvesting at a lower rate.

Government Bonds: This type of bond is issued by the governments and public sector bodies, in order to fund the ongoing operations and the fiscal deficit. Especially, when the tax revenues are not sufficient, governments prefer to fund long-term projects through bond issues. Governments mainly have three borrowing instruments:

- treasury bills which satisfy short-term financing needs,

- treasury notes that are mid-term debt instruments,

- government (treasury) bonds which are issued to satisfy long-term financing needs.

Government bonds can be issued discounted or with coupons, and their maturity can range between 1 and 30 years and its coupon rates are lower than the coupon rates of the company bonds, since the return of the bondholders are considered as risk-free return.

A corporate bond can be defined as the debt instrument issued by non-government borrowers. Corporate bonds are accepted as riskier compared to the government bonds, so the coupon rate of these instruments is higher than the government bonds. The main factor that determines the coupon rate of the corporate bonds is creditworthiness of the issuer.

The creditworthiness of the issuer reflects the default risk of the bond. For this reason, the bond investors should evaluate the creditworthiness of the corporation in an investment process. Coupon rates of corporate bonds are higher than the coupon rates of government bonds since the possibility of default in these bonds is higher compared to government bonds.

Debenture (Unsecured) Bonds, Secured Bonds and Guaranteed Bonds: Debenture bonds are unsecured bonds and payments of these bonds depend on the general credit strength of the issuer. The holders of these bonds are accepted as general creditors of the issuer. Unlike the holders of debenture bonds, secured bondholders are protected against the default risk via the right to sell the pledged asset. Therefore, a secured bond can be defined as the bond that is secured by a pledge asset of the issuer. These bonds also can be secured with the revenue that arises from the project, for which the bond was issued to provide finance.

Guaranteed bond is a bond issued by a company and guaranteed by another corporation or corporations. The default risk is, therefore, transferred from the bondholder to the guarantor. In the event of default, interest and principal payments of guaranteed bondholders are paid by the guarantor such as banks, insurance companies and governmental agencies.

Floating-Rate Bonds: The coupon rate of these bonds change depending on a reference rate. One of the most widely used benchmarks for floating rate is the LIBOR (London Interbank Offered Rate), which is the borrowing rate in the London Interbank Market. Another reference rate is the Prime Rate, which is the interest rate that banks charge their most creditworthy customers.

Index-Linked Bonds: Index-linked bond is a bond that the coupon payments and in some issues principal payments are linked to a specific index such as Consumer Price Index (CPI).

Callable and Puttable Bonds: Callable bonds provide the issuer the opportunity of buying his debt prior to the scheduled maturity date in case interest rates fall below the coupon rate of the bond.

A puttable bond is a bond that provides the holder to sell the bond back to the issuer at par on stated dates in theindenture. Put provision provides advantage to the holder, if the interest rates exceed the coupon rate.

Eurobonds and Foreign Bonds (International Bonds): Eurobond is a bond denominated in a currency that is different from the currency of the country where the bond is issued. They are typically issued by governments, large corporations and international institutions. For example, a bond denominated in US dollars and sold in London is a Eurobond. Foreign bond is a type of bond that is issued by a foreign company or foreign government. They are denominated in the currency of the country where they are sold. Some of the foreign bonds have specific names. For example, bonds issued in the United States by a foreign company are called Yankee Bonds, the foreign bonds issued in the United Kingdom are called Bulldog bonds (Maple bonds – Canada; Panda bonds – China; Samurai bonds – Japan; Rembrandt bonds - the Netherlands; Kiwi bonds – New Zealand; Matador bonds – Spain; Kangaroo or Matilda bonds Australia).

Convertible Bonds: Some of the bonds issued by corporations provide to the holder the right of changing the bond with another asset. These bonds are called convertible bonds. For example, holder of a convertible bond can be granted to receive the face value in cash or a unit of ordinary stocks of the issuer. This right can be used at maturity or over a specified period depending on the indenture.

Bond Valuation

The concept of time value of money must be understood to calculate the cost of funds, the value of the investments and the yield on an investment such as bonds.

Time value of money is a critical concept in understanding many fields of finance. The value of financial instruments and future cash flows of investments is determined by discounting, and future value of money resulting from an investment is calculated by compounding. Time value of money in the easiest way can be defined with the sentence “$1 you have today is more valuable than the $1 that you will have in the future”. Today’s $1 is more valuable because you may make an investment with this money and obtain interest on it. Therefore, you can have more than $1 after a while. Yet, this is valid as long as the interest rate is strictly positive.

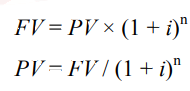

The formulas of compounding (future value) and discounting (present value) are as follows;

Present value of cash flow, is the annual interest rate (yield) and is the number of years for which compounding or discounting is done. If the cash flows occur different than annual frequency, and must be revised. For example, for semiannual periods is divided to 2 and is multiplied by 2, since there are two semiannual payments in a year.

The discount factor that is used in bond valuation consists of a risk-free rate and a risk premium. Risk-free rate refers to the coupon rate of government bonds, and the risk premium includes economic, industrial and firm level risks. In this context, the factors that affect the discount rate. Hence the bond value are as follows:

- The economic outlook,

- Monetary policy of the country,

- Government’s borrowing needs,

- Inflationary expectations,

- The level of economic activity, important

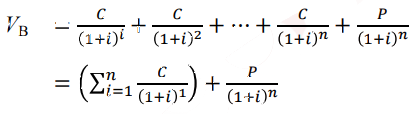

In general, value of a bond can be estimated by the following formula;

Here,

- V B is the value or price of the bond,

- C is the coupon payment,

- i is the coupon or interest rate,

- n is the number of periods until the maturity,

- P is the principal or par value of the bond.

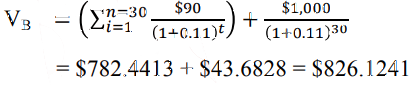

Assume a 30-year bond with a par value of $1,000, the coupon rate of the bond is 9%, therefore, the coupon payments will be $90 ($1,000 x 0.09), If the discount rate is 11%, the value of the bond is:

A zero-coupon bond provides the investor a cash flow equal to the par value, which will be obtained at maturity. Therefore, the value of a zero-coupon bond is equal to the present value of the bond’s par value and it can be estimated by the following formula:

Assume a 5-year zero-coupon bond which has $1,000 par value. If the required return is 8%, the price of the bond should be:

Coupon payments of bonds can be settled annually or semiannually. If the interest payments will be made semiannually, then the annual coupon interest payment and discount rate must be divided to 2, and the maturity should be multiplied by 2. Therefore, the valuation formula can be revised for semiannual coupon bonds as follows:

There are different yield concepts with respect to bonds. In this context, the concepts of nominal yield, current yield, yield to maturity and yield to call are defined below:

- Nominal Yield: Nominal yield of a bond is the coupon rate of the bond, and it does not take into consideration the bond’s time to maturity or market price of the bond. For example, the nominal yield of a bond with a 10% coupon rate is 10% (0.10), whether it is sold at par or not and matures in 2 or 30 years.

- Current Yield: Current Yield is the return an investor expects to earn from an investment or financial instrument.

- Yield to Maturity (YTM): There are several measures, which are used to evaluate the return of bonds. One of these measures is yield to maturity, which can be also calculated for the callable and putable bonds. YTM is the rate, which equates the bond price to the present value of its future cash flows, and it is a measure of the growth rate of the investment. YTM of a bond is the internal rate of return of a bond.

- Yield to Call (YTC): Sometimes, those in need of funds may issue bonds that give the issuer the right to call back. In this case, yield to call is an appropriate measure to evaluate the return of the bond. YTC is the rate that equals the present value of the expected cash flows of the bond to the price plus accrued coupon payments.

Risk of Bond Investments

Like other investments, bond investments carry risks. Besides the risks that arise from the economic conditions, bond investments carry specific risks such as call risk and downgrade risk.

The main risk associated with the bond investment is default risk. Default risk refers to the possibility that the issuer fails to make the payments of the bond. Another risk important for the bondholders is interest rate risk. Changes in the interest rates are important because they directly affect the price of the bond. There are also risks such as currency risk, which depends on the type of bond, undertaken by the bondholder.

Default Risk (Credit Risk): Default risk is the risk that the borrower will not meet the obligation at the agreed time. For bonds, default risk refers that the issuer will fail to make interest payments and/or principal at the determined dates. When the issuers default, the bondholders can sue for bankruptcy, if the issuers do not file for bankruptcy.

Downgrade Risk : Downgrade risk can be defined as the risk that the rating of the issuer or instrument will be downgraded by a rating agency or more rating agencies, due to the deterioration in the creditworthiness of the borrower. Therefore, the downgrade risk can be considered as a component of credit risk. However, the origin of the downgrade risk is generally an event notably default, and it is estimated depending on the possibility of this event.

Interest Rate Risk or Market Risk: Interest rate risk refers to potential losses caused by changes in the interest rates. The interest rate changes are important especially for the investors who plan to sell the bond before the maturity date. If the interest rates increase, the investor will sell the bond at a lower price. This risk undertaken by the investor is called interest rate risk or market risk, and it is one of the most important risks of fixed income investments.

Call Risk: Call risk is a type of risk that some bonds are exposed to. Call risk is the possibility that the issuer will buy back the bond before the maturity date. The bondholders undertake this risk if the bond carries a call provision.

Reinvestment Risk: Investors desire to reinvest their income generated from their investments. In this case, they are faced with the reinvestment risk that arises from the possibility of reinvesting their money at lower rates. This risk is high when the interest rates are volatile. Especially for bond investments, reinvestment risk is higher because the price of the bond decreases as the interest rates increase, and the bondholders sell their bonds at lower prices besides reinvesting their money at lower rates.

Currency Risk (Foreign Exchange Risk): In general terms, currency risk can be defined as the potential loss occurs due to the changes in the exchange rates. The bondholders undertake currency risk when they invest in a bond which pays the coupons and principal in a foreign currency. When the foreign currency that the bondholders will receive as the cash flows of the bond depreciates against the domestic currency, it will take more foreign currency to buy the same amount of domestic currency.

Purchasing Power Risk or Inflation Risk: This type of risk is associated with the unanticipated changes in the future value of money. Investors who want to protect their investment against this contingency can buy index-linked securities, for which the payoffs are adjusted according to the price changes.

Duration and convexity are tools that are widely used to manage the risk exposure of fixed-income investments like bonds.

Duration is a first order interest rate risk measure and it reflects the sensitivity of the bond to changes in interest rate rates. Duration is a method that gives a weighted average of the time to receive the investment, which uses the present value of cash flows gained from the bond. Besides the principal of the bond, it considers the coupon payments and the timing of these payments. In this context, duration can be defined as the average time that is needed to receive principal and coupons of the bond, which considers the sensitivity of bond to interest rate changes.

Duration is a measure of interest rate sensitivity of bond and gives the weighted average time to receive the cash flows of the bond. İmportant. Duration decreases when the interest rates increase. Duration of a bond with higher coupon rate is shorter than the duration of a bond with lower coupon rate.

Duration is also known as “ Macaulay Duration ” since the concept of duration was firstly developed by Frederick Macaulay. Macaulay duration is calculated by multiplying the time (t) until the receipt of cash flows with the present value of cash flows, and then dividing the sum of these values to the sum of present value of cash flows (PVCF). For bonds with semi-annual coupons, the cash flows are discounted at half of the discount rate. Macaulay duration formula can be shown as follows:

There are many forms of duration focusing on different properties of bonds, which have been developed to evaluate different types of bonds. One of these forms is modified duration. While duration or Macaulay duration reflects the sensitivity of a bond to the interest rate changes, modified duration evaluates the effects of yield changes on the price of the bond. Modified duration is calculated under the assumption that cash flows of the bond do not change when the yield changes. For this reason, this measure is not suitable for some types of bonds such as callable bonds and bonds with embedded.

In the formula, k is the number of coupon payments per year. For example, k is 1 for bonds that make annual coupon payments, and k is 2 for bonds that make coupon payments semi-annually.

Duration is a first order interest rate risk measure, which uses first-order derivatives. However, convexity uses second-order derivatives and represents a second order interest rate risk. Duration does not consider the convexity of bond price with respect to interest rates and estimates the approximate percentage of price change regardless of the way of the change in the interest rate. Yet, for large changes in the interest rates, the magnitude of price changes is different for increases and decreases. For this reason, duration is a good measure to analyze the effects of small interest rate changes on the bond price, whereas it is not a suitable measure in cases where interest rate changes are large. For these cases, convexity is the appropriate measure to evaluate the interest rate risk.

Convexity, in fact, shows by how much the duration of a bond will change, when interest rates change and it measures the volatility of the duration. The convexity of a bond can be calculated by the following formula:

Lenders want to evaluate creditworthiness or repayment ability of the borrowers. They decide if they will fund the borrower or not depending on the repayment ability. On the other hand, cost or interest rate of the debt is fundamentally determined by the repayment ability. As with lenders, investors also consider the creditworthiness of the issuer. They decide if they purchase the security or not by evaluating the default risk of the issuer. For bond investors, credit rating is a suitable indicator in order to evaluate the default risk of the issuer. Issuers also want to have credit ratings in order to increase the marketability of their bonds, since ratings reflect trustworthiness of issuers and it is an important process for investors.

Several rating agencies such as Standard & Poor’s, Moody’s and Fitch rate corporate and government bonds with respect to the issuer’s ability to make the regular coupon payments and principal payment at the maturity date. The agencies monitor the issuers and change the rating if the credit quality changes. If the credit quality of the issuer improves, then the agency upgrades the rating, and if the credit quality of the issuer deteriorates, then the agency downgrades the rating. The rating agencies also modify the ratings by additional expressions such positive, developing, stable or negative. While positive outlook indicates a possible upgrading in the future, the negative outlook gives the signal of a possible downgrading in the future.